The content draws on the canonical academic formulation and on international guidance documents that shape modern expectations for firms. It aims to be neutral and factual, with pointers to primary standards and policy sources.

What is meant by the responsibility of business to the society: definition and context

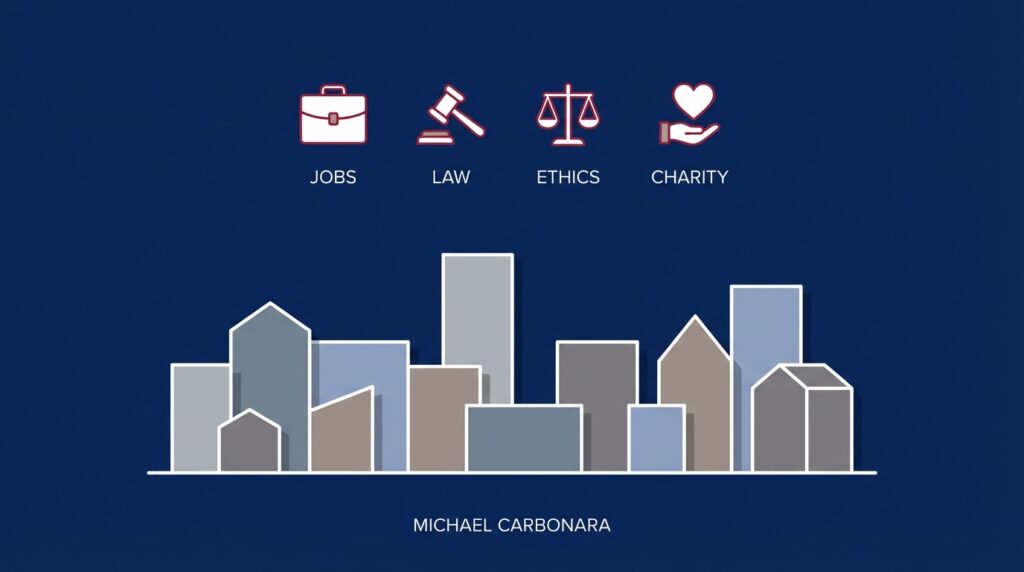

The responsibility of business to the society is commonly described by a four-part corporate social responsibility framework that lists economic, legal, ethical and philanthropic duties, a structure first set out by Archie B. Carroll in 1991 and still cited in scholarship and guidance Carroll 1991.

In practical terms, the phrase responsibility of business to the society helps voters and civic readers separate what firms are primarily expected to do by law and market function from what they may choose to do for broader community benefit.

Knowing this framework matters because it provides a shared language for discussing regulation, corporate reporting and local impacts on jobs and services.

Businesses have four commonly cited responsibilities: to be economically viable and provide goods and jobs, to comply with legal obligations, to meet ethical expectations beyond the law, and to make discretionary philanthropic contributions.

At a glance, the four roles are:

1. Economic: produce goods and services, create jobs and generate wealth.

2. Legal: comply with laws, regulations and formal obligations.

3. Ethical: meet broader societal expectations beyond legal minimums.

4. Philanthropic: discretionary community contributions such as donations or volunteering.

That short list is the canonical description used in both academic discussion and policy advice, and it is a useful starting point for voters who want to assess how businesses in their district act and report.

Origins of the four-role framework and modern guidance

Archie B. Carroll’s 1991 article formalized the pyramid model that arranges economic, legal, ethical and philanthropic responsibilities into a single framework, and scholars and practitioners continue to use this arrangement as a baseline reference Carroll 1991 and the ScienceDirect entry https://www.sciencedirect.com/science/article/pii/000768139190005G.

Since Carroll’s work, international guidance has developed to interpret and operationalize parts of the framework for different audiences and jurisdictions.

ISO 26000 provides practical guidance on social responsibility and is commonly cited when firms and stakeholders discuss ethical expectations that go beyond legal compliance ISO 26000 guidance.

At the same time, instruments such as the OECD Guidelines for Multinational Enterprises explain expectations for firms operating across borders, and regional policy work by actors such as the European Commission situates economic duties alongside legal and ethical obligations OECD Guidelines.

These documents do not replace national law, but they are used by companies, policy makers and civil society to align practice with evolving expectations about social performance.

Economic role: producing value, jobs and goods

The economic role of business – producing goods and services, creating jobs and generating wealth – is treated as the primary responsibility in classical CSR literature, and that priority is reflected in contemporary policy guidance that recognizes firms first as economic actors European Commission CSR guidance. See also a practical guide Diligent.

For local voters, the economic role matters because it connects business activity to employment, local supply chains and the tax base that supports public services. Observing how a firm’s core operations affect jobs and local purchases is a concrete way to assess economic responsibility without turning to technical reports.

Policy documents often treat the economic role as the foundation on which other duties rest; proponents of the four-part model argue that businesses must be economically viable to meet legal, ethical and philanthropic commitments in a lasting way.

In practical terms, decisions about where to locate a facility or how to structure wages and procurement influence whether a firm meets its economic responsibilities to a community.

Legal responsibilities: compliance and formal obligations

Legal responsibilities refer to compliance with laws, regulations and formal obligations that apply to a firm’s operations, and international instruments like the OECD Guidelines help clarify expectations for companies that operate in more than one country OECD Guidelines.

Legal duties set the baseline that firms must meet before ethical or voluntary activities are considered; this distinction is important for civic readers who want to know whether a firm is meeting its required obligations in areas such as employment law, environmental permits or product safety.

Regulatory frameworks also influence reporting duties: in recent years regulators and standard-setters have increased emphasis on disclosure of social and environmental performance, even as standardized measurement methods remain under development European Commission CSR guidance.

When evaluating firms, voters can check public filings and regulatory records to confirm legal compliance rather than relying on marketing statements.

Ethical responsibilities: going beyond what the law requires

Ethical responsibilities cover actions aligned with societal norms and stakeholder expectations that are not strictly required by law; guidance like ISO 26000 frames how organizations can approach those responsibilities in practice ISO 26000 guidance.

Voluntary initiatives, for example the principles put forward by multinational voluntary efforts, give companies practical reference points for managing human rights, labor practices and community engagement even where the law does not set explicit requirements UN Global Compact mission and principles.

Ethical duties can create reputational incentives: firms that act consistently with stakeholder expectations can reduce risk and build trust, while inconsistent behavior can lead to criticism even if a company remains technically compliant with law.

Philanthropic role and the move toward shared value

In Carroll’s model, philanthropic responsibilities are discretionary activities such as donations, sponsorships and employee volunteering; these efforts sit at the top of the pyramid and are not required in the same way economic and legal duties are Carroll 1991.

A short checklist to help firms align charitable activities with core business contributions

Keep items proportionate to firm size

Recent business literature has highlighted shared-value thinking, which encourages firms to design philanthropic or social programs that also connect to the company’s capabilities and market roles, though the degree of integration varies across sectors and firms Creating Shared Value and further perspectives are discussed in the literature review.

For civic readers, the distinction matters: a firm’s philanthropic spending may be generous, strategic, or both, and understanding the intent and link to core operations helps voters assess whether charitable actions are additive or primarily promotional.

Reporting, accountability and the state of measurement

Since the early 2020s, regulators, standard-setters and multilateral bodies have stepped up work on disclosure and accountability for social performance, prompting renewed attention to how firms report on the four responsibilities and to what counts as adequate evidence OECD Guidelines.

That renewed emphasis has not yet produced universal, standardized metrics; standard-setting debates continue about how to balance useful comparability with the practical burdens of reporting for smaller firms European Commission CSR guidance.

Explore primary guidance on business responsibility

For readers who want primary sources on disclosure and international expectations, consult the OECD Guidelines, ISO 26000 and regional CSR guidance documents directly for full texts and implementation notes.

Smaller businesses often report informally or use scaled approaches, which can make cross-company comparison difficult. Voters should consider both the presence of disclosure and the quality of measurement when assessing claims.

How to decide priorities: a practical decision framework for businesses

A neutral, stepwise framework helps explain how firms set responsibility priorities: first satisfy legal obligations, then ensure economic viability, next consider ethical alignment and finally decide on voluntary philanthropic activities, with each step informed by stakeholder assessment and relevant guidance ISO 26000 guidance.

Concretely, the checklist looks like this: confirm legal compliance, assess how proposed actions affect core business value, consult key stakeholders, and scale voluntary programs to capacity. International tools such as OECD guidance can help structure cross-border considerations OECD Guidelines.

Smaller firms may use proportionate approaches, focusing on a few measurable actions rather than extensive formal reporting, to avoid disproportionate compliance costs while still addressing community expectations.

Common mistakes and pitfalls to watch for

Common mistakes and pitfalls to watch for

A common mistake in public discussion is to treat slogans or marketing as evidence of substantive responsibility; without supporting disclosure or primary filings, promotional language can overstate the depth of corporate efforts OECD Guidelines.

Relatedly, disclosure without clear measurement can create a false sense of accountability; standard-setting bodies continue to work on consistent metrics because partial reporting can mask performance differences among firms European Commission CSR guidance.

When evaluating claims, readers should look for primary sources such as public filings, NGO reports and the original standards documents rather than relying solely on company summaries.

Practical examples and concluding takeaways for voters

Practical examples and concluding takeaways for voters

Small retailer scenario: a local shop meets its economic responsibility by keeping regular hours and employing local staff, meets legal duties by following local health and safety rules, addresses ethical expectations by sourcing responsibly, and engages philanthropically through occasional local donations, illustrating how the four roles can co-exist in a small-business setting Carroll 1991.

Regional manufacturer scenario: a plant’s economic role is central to employment in its town, legal compliance includes environmental permits, ethical considerations may involve supply-chain labor practices, and philanthropy might involve workforce training programs connected to long-term community benefit OECD Guidelines.

National firm scenario: a large company may face cross-border legal and ethical expectations shaped by OECD and ISO guidance, and its philanthropic activities may be evaluated for how well they align with core business strategy and measurable community outcomes ISO 26000 guidance.

For voters in Florida’s 25th District and elsewhere, the practical takeaway is to use the four-role framework as a checklist when assessing business behavior: ask about jobs and economic impact, verify legal compliance, look for ethical practice beyond the law, and evaluate whether charitable efforts are substantive or mainly promotional.

The four roles are economic (produce goods and jobs), legal (follow laws), ethical (meet societal expectations beyond law) and philanthropic (voluntary community support).

ISO 26000 is guidance on social responsibility that helps organizations interpret ethical duties and stakeholder expectations, but it is voluntary and does not replace law.

Check primary sources such as public regulatory filings, company disclosures that reference standards, and guidance documents from bodies like the OECD or ISO.

References

- https://doi.org/10.1016/0007-6813(91)90005-8

- https://www.iso.org/iso-26000-social-responsibility.html

- https://mneguidelines.oecd.org/

- https://commission.europa.eu/business-economy-euro/doing-business-eu/corporate-social-responsibility-csr_en

- https://michaelcarbonara.com/contact/

- https://michaelcarbonara.com/

- https://www.unglobalcompact.org/what-is-gc/mission

- https://hbr.org/2011/01/the-big-idea-creating-shared-value

- https://www.sciencedirect.com/science/article/pii/000768139190005G

- https://journals.sagepub.com/doi/abs/10.1177/00076503211001765

- https://www.diligent.com/resources/blog/corporate-social-responsibility-csr

- https://michaelcarbonara.com/news/

- https://michaelcarbonara.com/about/